Imagine a world where your grocery bills, charity donations, and even your subscription services are visible to the federal government in real time. This isn't a dystopian novel plot; it is the operational reality of Central Bank Digital Currencies (CBDCs), which are digital versions of fiat currencies issued directly by central banks. While tech enthusiasts often debate Bitcoin or Ethereum, governments worldwide are quietly building infrastructure for something far more impactful for state power: their own digital cash.

For governments, the shift from physical cash to digital sovereign currency offers unprecedented leverage. It is not just about faster payments or lower printing costs. It is about total visibility and control over the economic behavior of every citizen. If you are trying to understand why nations like China have rushed to launch these systems while others hesitate, you need to look at the specific advantages they provide to the state. Here is how CBDCs transform governance, monetary policy, and social control.

The End of Anonymity: Real-Time Financial Surveillance

The most immediate benefit for any government adopting a Central Bank Digital Currency is the elimination of anonymous transactions. Physical cash has always been the ultimate tool for privacy. You can buy anything with paper money without leaving a digital trail. A CBDC removes this shield entirely. Every transaction made with a digital currency leaves a permanent, immutable record on a centralized ledger controlled by the central bank.

This means that financial surveillance becomes the continuous monitoring of individual spending patterns and financial activities by government authorities. According to analysis from The Policy Circle, this allows federal governments to monitor citizen spending patterns with granular detail. They can see exactly what you buy at the grocery store, which nonprofits you donate to, and what subscriptions you maintain. This data creates comprehensive financial profiles for every user, linking them to national digital identity systems.

Consider the implications for law enforcement and regulatory bodies. Unlike private crypto wallets, which can offer varying degrees of anonymity depending on the coin, a CBDC is inherently tied to your legal identity. This traceability enables central banks to monitor all monetary operations within their ecosystem instantly. For a government, this is a powerful tool for tracking illicit activity, but it also raises serious concerns about civil liberties. The Cato Institute warns that this level of oversight could spell the end of financial privacy, enabling state tracking of personal habits and raising significant First and Fourth Amendment issues in democratic societies.

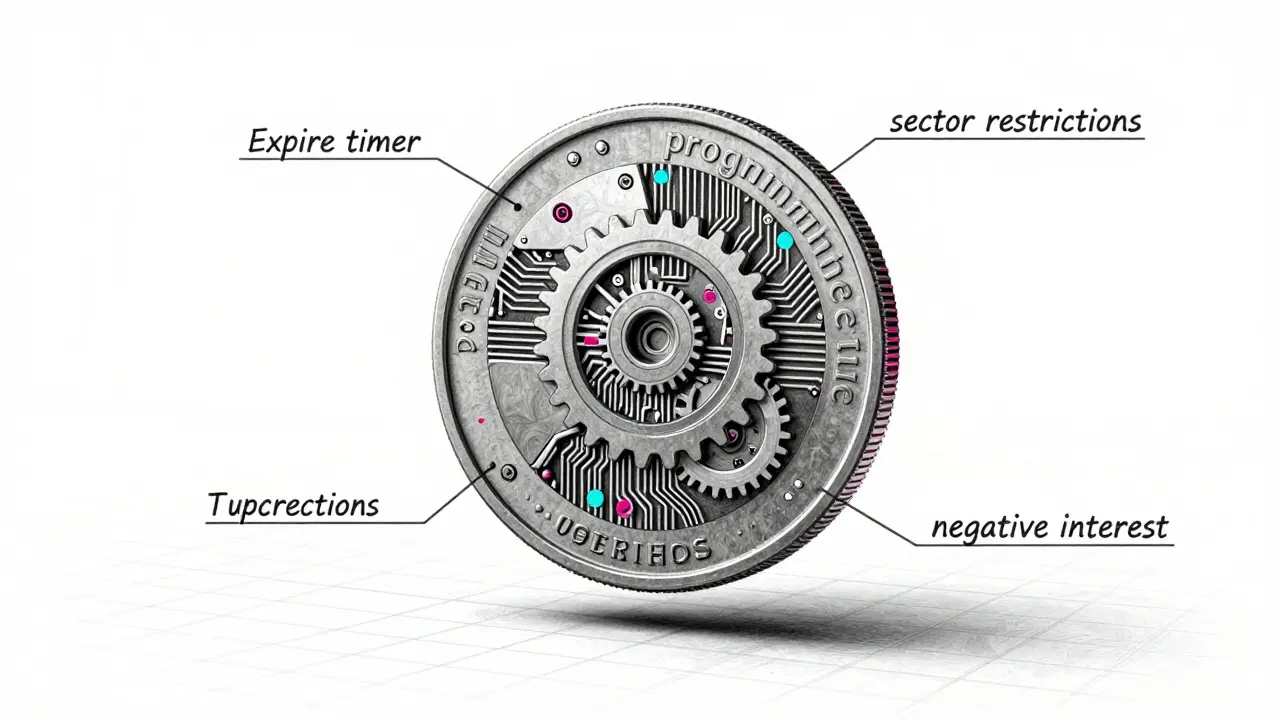

Programmable Money: Directing Economic Behavior

One of the most radical features of a Central Bank Digital Currency is its programmability. Traditional cash is "dumb" money; once you hold it, you can do whatever you want with it. A CBDC can be "smart" money. Governments can embed rules directly into the code of the currency itself, allowing them to dictate how, when, and where funds can be spent.

This capability allows for precise monetary policy implementation. During an economic downturn, a central bank might issue stimulus checks. With a CBDC, they could program these funds to expire after 30 days if not spent, forcing citizens to inject money back into the economy immediately rather than saving it. They could restrict usage to specific sectors, such as local businesses or renewable energy providers, ensuring the stimulus hits targeted areas.

Negative interest rates become a monetary policy tool where central banks charge commercial banks for holding reserves, encouraging lending and spending. Implementing negative interest rates has historically been difficult because people simply withdraw cash and store it under mattresses to avoid fees. With a CBDC, there is no physical cash to hoard. Central banks can debit accounts directly, maintaining greater control over money circulation and interest rate alterations. This permits the ready use of unconventional policy instruments to induce economic growth or curb inflation with surgical precision.

China's Model: Social Credit and State Control

To understand the full extent of governmental benefits, we must look at China's digital yuan, which is the People's Bank of China's official digital currency integrated with state surveillance systems. China provides the clearest example of how CBDCs can be used for social control. Analysis from Burr.com indicates that the digital yuan is tightly linked to the country's social credit system. The Chinese Communist Party uses this currency to view users' financial data, censor activity, and direct spending through time limits and purchase restrictions.

In this model, the CBDC acts as an extension of internet access control mechanisms. If a citizen's social credit score drops, their ability to spend digital yuan could be restricted. They might be blocked from buying high-end electronics, booking flights, or donating to certain organizations. This increases the state's ability to implement social compliance through financial mechanisms. For governments seeking to enforce behavioral norms, a CBDC offers a lever that is far more effective than traditional policing or propaganda.

Observers warn that this opens new forms of government surveillance. The combination of real-time financial data and social scoring creates a feedback loop where financial behavior influences civic privileges, and vice versa. While Western democracies may not adopt such extreme measures initially, the technical infrastructure to do so would exist from day one of CBDC implementation.

Operational Efficiency and Cost Reduction

Beyond control and surveillance, CBDCs offer tangible operational benefits. Printing, distributing, securing, and destroying physical currency is expensive. The Federal Reserve and other central banks spend billions annually on these logistics. A digital currency eliminates the need for physical infrastructure. There are no minting costs, no armored truck transports, and no vault security expenses.

Transaction efficiency sees a massive boost as well. Current cross-border transactions often take one to five days and involve multiple intermediaries, each adding fees. The Bank for International Settlements notes that CBDCs could reduce these costs significantly by removing money transfer operators. According to World Bank data, migrants currently face an average charge of 6.25% when sending remittances. A standardized CBDC system could streamline these transfers, making them instantaneous and nearly free.

Domestically, settlement times shrink from days to seconds. This improves liquidity management for businesses and reduces the friction in daily commerce. For the government, this means a more responsive financial system that can adapt quickly to economic shocks. Swift payment provider research highlights that current real-time payment methods face interoperability issues due to non-standardized systems globally. CBDCs could resolve this by providing a unified, government-backed standard.

Financial Inclusion and Direct Citizen Payments

Governments often cite financial inclusion as a primary reason for developing CBDCs. Approximately 1.4 billion adults worldwide remain unbanked, lacking access to formal financial services. A CBDC could extend banking services to these populations without requiring traditional brick-and-mortar branches. Users only need a smartphone or a basic digital wallet to participate in the formal economy.

This capability was highlighted during recent global crises. The World Economic Forum noted that CBDCs could have assisted governments with direct energy bill support payments prompted by soaring gas prices. Instead of relying on intermediary banks and payment processors, which add administrative costs and delays, governments can transfer funds directly to citizens' digital wallets. This ensures that aid reaches recipients quickly and transparently, reducing fraud and leakage in welfare programs.

However, this convenience comes with a trade-off. To receive these benefits, citizens must enter the digital financial ecosystem, thereby surrendering their anonymity. The unbanked population gains access to modern finance but loses the privacy that cash previously provided. For governments, this expands their tax base and regulatory reach into previously informal sectors of the economy.

Combating Illicit Finance and Tax Evasion

Regulatory and compliance benefits are substantial for any jurisdiction. Cash is the preferred medium for money laundering, tax evasion, and funding illegal activities because it is hard to trace. A CBDC creates a permanent digital record for every transaction, enabling law enforcement to track the flow of funds with unprecedented accuracy.

This enhances the ability to fight fraud and illicit activity. Authorities can identify suspicious patterns in real time, flagging transactions that deviate from normal behavior. This surveillance capability extends to implementing capital controls, taxation enforcement, and economic sanctions with precision. For example, if a country wants to prevent capital flight during a crisis, it can easily restrict outbound transfers via the CBDC platform.

Tax collection becomes more efficient as well. Since all transactions are recorded, tax authorities can automatically calculate liabilities based on actual spending and income data. This reduces the burden of manual reporting and minimizes opportunities for underreporting. For governments struggling with budget deficits, this represents a significant revenue opportunity.

Political Resistance and Privacy Concerns

Despite these benefits, the push for CBDCs faces significant political headwinds, particularly in liberal democracies. In the United States, congressional opposition has grown. Representative Tom Emmer (R-Minnesota), Senator Mike Lee (R-Utah), and Senator Ted Cruz (R-Texas) have introduced legislation to ban government CBDCs. Florida Governor Ron DeSantis has also voiced strong concerns, indicating state-level resistance to federal digital currency implementation.

The core of this opposition lies in the fear of abuse. Expert analysis from the Cato Institute suggests that government officials and their cronies stand to benefit most from CBDC implementation, while the broader public may pay the price in lost freedom. The potential for misuse is high. If a government can freeze assets, restrict spending, or monitor every purchase, the balance of power shifts dramatically away from the citizen.

Nigeria's experience with the eNaira illustrates adoption challenges. Despite being one of the first countries to launch a CBDC, Nigeria faced low uptake due to mistrust and limited infrastructure. Citizens were wary of giving the government such intimate access to their finances. This highlights a critical barrier: trust. For a CBDC to succeed, the population must believe that the government will not abuse its powers. In regimes with poor human rights records, this trust is nonexistent.

| Feature | Physical Cash | Central Bank Digital Currency (CBDC) |

|---|---|---|

| Anonymity | High (Untraceable) | None (Fully Traceable) |

| Programmability | Not Possible | High (Time/Place Restrictions) |

| Monetary Policy Speed | Slow (Indirect) | Instant (Direct Account Access) |

| Surveillance Capability | Low | Total (Real-Time Monitoring) |

| Cost of Issuance | High (Printing/Security) | Low (Digital Infrastructure) |

The Future of Government Power

The future of governmental finance is moving toward digital integration. The combination of real-time financial surveillance, direct citizen account access, and programmable money features provides tools for social and economic control that surpass any historical precedent. While the operational efficiencies and financial inclusion arguments are valid, the underlying driver for many governments is the desire for enhanced oversight.

As technology advances, the line between monetary policy and social engineering will blur further. Citizens will need to weigh the convenience of instant, secure payments against the loss of financial privacy. For governments, the choice is clear: CBDCs offer a path to total economic visibility. Whether this leads to better governance or increased authoritarianism depends largely on the legal frameworks and cultural values of each nation.

What is the main benefit of CBDCs for governments?

The primary benefit is enhanced financial surveillance and control. CBDCs allow governments to monitor all transactions in real time, eliminating the anonymity of cash and enabling precise implementation of monetary policies, such as negative interest rates and targeted stimulus spending.

Can CBDCs be used to restrict spending?

Yes. Because CBDCs are programmable, governments can embed rules into the currency. This includes setting expiration dates on stimulus funds, restricting purchases to specific categories or geographic regions, and preventing hoarding by charging fees for large balances.

How does China use its digital yuan for social control?

China links its digital yuan to its social credit system. The government can monitor financial behavior and restrict spending capabilities for individuals with low social scores. This allows the state to enforce compliance by limiting access to essential services and luxury goods based on financial and behavioral data.

Do CBDCs improve financial inclusion?

Potentially yes. CBDCs can provide banking services to unbanked populations without the need for traditional bank branches. However, this comes at the cost of privacy, as users must register with their legal identities to access the digital currency system.

Why are some US politicians opposing CBDCs?

Politicians like Senators Mike Lee and Ted Cruz oppose CBDCs due to concerns over government overreach and privacy violations. They argue that a digital currency gives the federal government too much power to monitor and control individual financial activities, potentially leading to censorship and asset freezing.

Are CBDCs safer than cryptocurrencies?

From a stability perspective, yes. CBDCs are backed by the government and do not suffer from the volatility of cryptocurrencies like Bitcoin. However, they lack the decentralization and privacy protections that many crypto users value, making them vulnerable to state interference and surveillance.