Gridex (GDX) vs AMM DEX Comparison Calculator

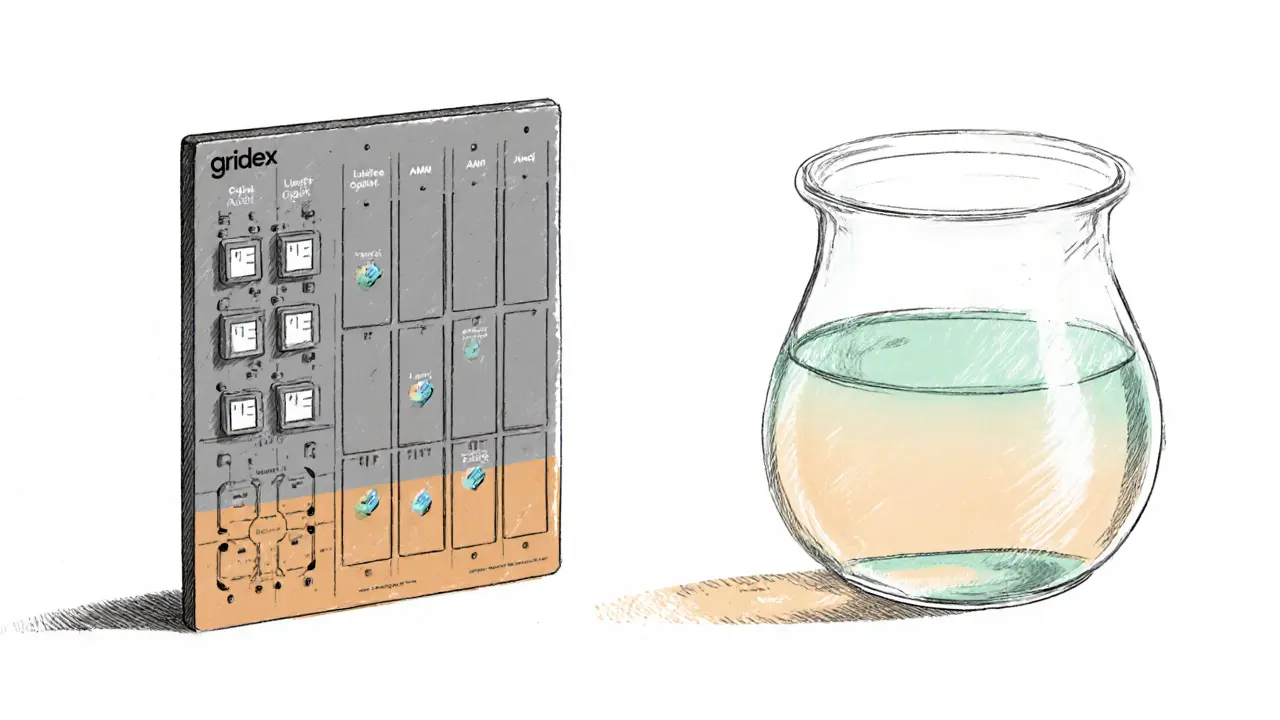

Liquidity Model: Order-book (limit orders)

Gas Cost: ~50-70 gwei

Slippage for large trades: Low - price set by order

Impermanent loss risk: None - no liquidity provision

Upgradeability: Non-upgradable contracts

Current Market Adoption: Very low - minimal volume

Liquidity Model: Liquidity pools (constant product)

Gas Cost: ~45-65 gwei

Slippage for large trades: High - pool depth limits size

Impermanent loss risk: Present - LPs exposed to price shifts

Upgradeability: Upgradeable via proxy patterns

Current Market Adoption: High - billions of daily trades

| Attribute | Gridex (GMOB) | AMM (e.g., Uniswap) |

|---|---|---|

| Liquidity Model | Order-book (limit orders) | Liquidity pools (constant product) |

| Gas Cost (average swap) | ~50-70 gwei (optimised matching) | ~45-65 gwei (pool interaction) |

| Slippage for large trades | Low - price set by order | High - pool depth limits size |

| Impermanent loss risk | None - no liquidity provision | Present - LPs exposed to price shifts |

| Upgradeability | Non-upgradable contracts | Upgradeable via proxy patterns |

| Current Market Adoption | Very low - minimal volume | High - billions of daily trades |

Gridex (GDX) offers an on-chain order-book experience, which can reduce slippage for large trades and eliminate impermanent loss, but lacks liquidity and market adoption.

AMM DEXs like Uniswap are widely adopted, offer deep liquidity, but may suffer from higher slippage and impermanent loss for traders.

Conclusion: Gridex is an experimental protocol with unique features but limited real-world utility due to lack of liquidity. AMMs dominate the market with proven reliability and depth.

When you hear the term Gridex, you might wonder whether it’s another meme token or a serious piece of DeFi infrastructure. In reality, Gridex (GDX) is a decentralized trading protocol that tries to replace the usual liquidity‑pool model with a true order‑book system on Ethereum.

TL;DR - Quick Takeaways

- Gridex (GDX) runs on Ethereum and Arbitrum using a proprietary Grid Maker Order Book (GMOB) model.

- The token trades at under $0.08 with virtually no daily volume, reflecting limited market adoption.

- It is permissionless, non‑custodial and its smart contracts are non‑upgradable, meaning users keep control of assets but the protocol can’t evolve easily.

- Compared to AMM‑based DEXs, Gridex aims for lower gas costs while offering an order‑book experience.

- Community activity and developer updates are scarce, raising questions about long‑term viability.

What is Gridex (GDX) - Core Definition

Gridex (GDX) is a decentralized trading protocol that operates via smart contracts on the Ethereum blockchain, employing a proprietary Grid Maker Order Book (GMOB) model instead of the typical Automated Market Maker (AMM) approach. It was designed to be permissionless and non‑custodial, meaning users retain full control of their assets at all times.

Technical Backbone - How the Protocol Works

The most distinctive piece of Gridex’s architecture is the Grid Maker Order Book (GMOB) a hybrid order‑book system that attempts to match the efficiency of traditional exchange order books with the trust‑less nature of blockchain

Key technical points:

- Smart contracts on Ethereum: Gridex lives on the Ethereum mainnet, inheriting the network’s security guarantees. The contracts are deliberately non‑upgradable, locking in the code once deployed.

- Arbitrum deployment: To address Ethereum’s high gas fees, Gridex also runs on Arbitrum, an optimistic roll‑up that offers cheaper and faster transactions while still relying on Ethereum’s security.

- Order‑book vs. AMM: Unlike Uniswap or SushiSwap, which use liquidity pools, Gridex users place limit orders that sit in the GMOB until matched. This can reduce slippage for large trades and avoid the impermanent loss that liquidity providers face on AMMs.

- Gas cost parity: The protocol claims that maintaining an on‑chain order book does not significantly increase gas consumption compared with AMM swaps, thanks to a lightweight matching algorithm.

Where Can You Trade GDX?

Despite the innovative design, GDX’s market presence is extremely thin.

- MEXC a centralized exchange that lists GDX in its Innovation Zone, paired with USDT

- Coinbase provides price tracking for GDX but does not offer direct trading of the token

- CoinMarketCap aggregates pricing data from multiple sources, showing GDX at roughly $0.0789

The 24‑hour trading volume is effectively zero across all platforms, and the token’s circulating supply is listed as zero, creating a mismatch between market cap, TVL, and actual liquidity.

Gridex vs. Traditional AMM DEXs - A Quick Comparison

| Attribute | Gridex (GMOB) | AMM (e.g., Uniswap) |

|---|---|---|

| Liquidity Model | Order‑book (limit orders) | Liquidity pools (constant product) |

| Gas Cost (average swap) | ~50‑70gwei (optimised matching) | ~45‑65gwei (pool interaction) |

| Slippage for large trades | Low - price set by order | High - pool depth limits size |

| Impermanent loss risk | None - no liquidity provision | Present - LPs exposed to price shifts |

| Upgradeability | Non‑upgradable contracts | Upgradeable via proxy patterns |

| Current Market Adoption | Very low - minimal volume | High - billions of daily trades |

Tokenomics - What Powers GDX?

The GDX token serves three primary roles:

- Governance: Holders can vote on protocol parameters (e.g., fee structures) once a governance module is activated.

- Staking incentives: Early proposals mentioned reward programs for users who lock GDX to provide order‑book liquidity, though concrete details are scarce.

- Fee payment: Transaction fees on the platform are payable in GDX, potentially granting a revenue stream to token holders.

Because the smart contracts are non‑upgradable, any token‑level changes must be built into the original code, limiting flexibility. Supply‑side data is vague: total supply is around 200million tokens, but circulating supply is reported as zero on many trackers, making market‑cap calculations unreliable.

Regulatory Outlook - What Risks Exist?

Gridex operates as a permissionless, non‑custodial protocol, a design that generally avoids direct regulatory scrutiny. However, several gray areas remain:

- In jurisdictions that classify any on‑chain trading platform as a “exchange,” regulators might require licensing, even though Gridex does not hold user funds.

- Token‑based governance can be interpreted as a securities activity if the token is marketed as an investment vehicle.

- Cross‑chain deployment (Ethereum + Arbitrum) may expose the protocol to differing legal environments regarding roll‑up solutions.

Without a clear legal wrapper or compliance program, participants should treat GDX as a speculative asset.

Community and Development - Is Anything Happening?

One of the biggest red flags is the near‑absence of community chatter. Major platforms like Reddit, Discord, or Telegram show only a handful of members, and no official GitHub repository is publicly linked. The non‑upgradable contract architecture suggests that the core protocol has been “frozen,” which can be a security advantage but also means the team cannot push upgrades or bug fixes without deploying a new contract.

Because of this, price‑prediction services (e.g., CoinCodex) refuse to generate forecasts, citing insufficient historical data. The lack of a development roadmap further hampers investor confidence.

Should You Consider GDX? - Decision Checklist

- Risk tolerance: If you can stomach extreme volatility and near‑zero liquidity, GDX may be an experimental play.

- Use‑case fit: Traders looking for on‑chain limit‑order functionality might appreciate the GMOB model, but the current trade ecosystem is too thin to be practical.

- Long‑term outlook: Without clear community growth or developer activity, the protocol’s future is highly uncertain.

In short, only allocate money you’re prepared to lose and consider GDX more as a technology curiosity than a solid investment.

Frequently Asked Questions

What makes Gridex different from Uniswap?

Gridex runs an on‑chain order‑book (GMOB) where users place limit orders, while Uniswap uses liquidity pools that price swaps via a constant‑product formula. This means Gridex can offer lower slippage for large trades but suffers from almost no liquidity at the moment.

Can I earn fees by providing liquidity on Gridex?

Gridex does not have traditional liquidity providers because it does not use pools. Instead, the protocol may reward users who lock GDX to support the order book, but those incentive programs have not been officially launched.

Is GDX listed on any major exchanges?

The token is currently listed on MEXC’s Innovation Zone (GDX/USDT pair) and has price data on Coinbase and CoinMarketCap, but there is effectively zero trading volume across these platforms.

What are the risks of using a non‑upgradable smart contract?

Non‑upgradable contracts cannot be patched if a vulnerability is discovered, which adds a security risk. On the flip side, the code cannot be altered maliciously after deployment, offering certainty that the contract behavior won’t change.

How does Gridex handle transaction fees?

Fees are paid in GDX and are designed to be comparable to AMM fees on Ethereum. The exact rate is set within the smart contract and can be adjusted only by a governance vote (if the governance module is activated).