If you're thinking about launching a crypto exchange in Japan, you aren't looking for a simple checklist; you're looking at a full-scale organizational overhaul. Japan doesn't do "light" regulation. After the Mt. Gox disaster, the government decided that the only way to protect users was to build one of the strictest regulatory walls in the world. In Japan, operating without a license isn't just a grey area-it's illegal.

For those trying to enter the market, the Financial Services Agency is the primary financial watchdog responsible for overseeing the registration and operation of all crypto-asset exchange service providers (CAESPs). Known as the FSA, this agency ensures that any platform handling digital assets meets rigorous standards for capital, security, and corporate governance.

Quick Summary: Navigating the Japanese Market

- Mandatory Licensing: All exchanges must register with the FSA; operating without this is a criminal offense.

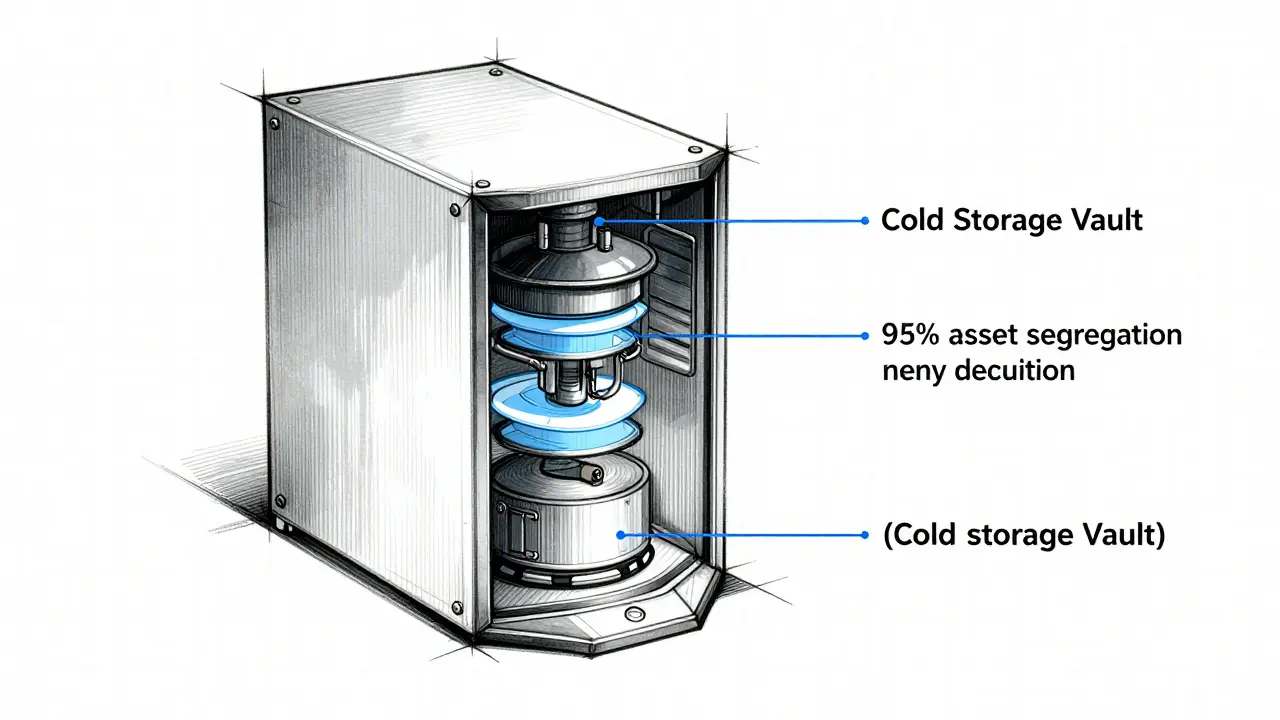

- Cold Storage Rule: A staggering 95% of customer assets must be kept in offline cold wallets.

- Local Presence: You cannot run a Japanese exchange from abroad; a local entity and physical office are required.

- Shifting Laws: Regulation is moving from the Payment Services Act toward the stricter Financial Instruments and Exchange Act.

- High Entry Bar: Expect high operational costs in exchange for a "quality stamp" that attracts serious investors.

The Legal Foundation: PSA vs. FIEA

To understand how crypto is governed in Japan, you have to look at two specific laws. For years, the Payment Services Act is the legislative framework that defines crypto-assets and mandates the registration of exchange services. The PSA treats crypto primarily as a means of payment, distinguishing it from traditional fiat currency.

However, the tide is shifting. As of 2026, the Financial Instruments and Exchange Act is the law governing securities and financial instruments, now increasingly applied to digital assets with investment or governance features. The FIEA is far more demanding than the PSA. Why the change? The FSA realized that many tokens act more like stocks than currency. By moving these assets under the FIEA, the government can enforce insider trading rules and mandatory disclosures, making the market feel more like a professional stock exchange and less like a digital wild west.

Hard Requirements for Registration

Getting a license from the FSA is a marathon, not a sprint. You can't just submit some paperwork and start trading. The regulator looks at the very DNA of your company.

First, you need a local legal structure. Most firms establish a Kabushiki Kaisha is a joint-stock company, which is the standard corporate form for businesses operating in Japan. Along with this, you need a physical office on Japanese soil and a domestic bank account. You can't bypass this with a virtual office; the FSA wants to know exactly where the people running the operation are located.

Financially, the barrier is high. You'll need a minimum capital of over 10 million yen, but that's just the baseline. The FSA will scrutinize your corporate governance and the qualifications of your managers. They aren't just checking if you have the money; they are checking if you have the expertise to manage risk without collapsing.

| Feature | Payment Services Act (PSA) | Financial Instruments & Exchange Act (FIEA) |

|---|---|---|

| Primary Focus | Payment and Utility | Investment and Securities |

| Asset Classification | Crypto-assets | Security Tokens / Financial Assets |

| Compliance Level | High | Extreme (Securities-grade) |

| Key Requirements | Registration, KYC, Asset Segregation | Disclosure, Insider Trading Controls |

The Cold Wallet Mandate: No Room for Error

If there is one thing the FSA is obsessed with, it's custody. They remember the horror of exchange hacks and have responded by mandating a a 95% cold storage rule. This means that 95% of all user funds must be kept in wallets that are completely offline. If you use a hot wallet for the remaining 5% to facilitate fast trading, you must back every single yen of those assets with your own company funds. This puts the risk entirely on the operator, not the customer.

This level of technical discipline is rare. In other countries, exchanges might promise "secure storage," but in Japan, this is a legal requirement with specific audits. If you can't prove your assets are offline, you can't stay in business. This technical rigor is why an FSA license is seen as a global "quality stamp." When a user sees that an exchange is FSA-registered, they know the assets aren't just being juggled in a hot wallet.

AML, KYC, and the Fight Against Scams

The FSA doesn't just care about where the coins are; they care about who is moving them. Japan has implemented some of the most rigorous Anti-Money Laundering is a set of laws and regulations intended to prevent criminals from disguising illegally obtained funds as legitimate income. The AML procedures are paired with strict Know Your Customer is the mandatory process of identifying and verifying the identity of a client when opening an account. KYC protocols that leave no room for anonymity.

The regulator is particularly focused on eliminating "investment scams" and inaccurate disclosures. They've seen too many whitepapers that promise the moon but deliver nothing. Now, the FSA scrutinizes these documents to ensure that investors aren't being misled by vague terminology or unrealistic profit projections. This focus on transparency extends to the DeFi space, where the FSA has created a dedicated Study Group to figure out how to regulate smart contracts without killing innovation.

Taxation: The Elephant in the Room

Despite the advanced regulatory framework, Japan's tax laws have historically been a major deterrent for retail traders. For a long time, crypto profits were taxed as "miscellaneous income," which could reach a staggering 55% when combined with local taxes. Compare that to the flat 20% tax on stocks, and it's easy to see why many traders felt penalized for choosing digital assets over traditional equities.

There is good news on the horizon. The FSA is currently pushing for tax reforms to align crypto assets with traditional financial instruments. The goal is to lower the burden on investors, which would likely trigger a massive surge in adoption as the "tax cliff" disappears. With adoption projected to hit over 15% of the population by 2026, these tax shifts are the final piece of the puzzle for a mature market.

Practical Implementation for New Entrants

If you're an international firm, don't expect a quick entry. You'll need to hire qualified Japanese compliance officers who understand the nuance of FSA expectations. The learning curve is steep because the FSA values the spirit of the law as much as the letter. They want to see a genuine commitment to user protection, not just a set of checkboxes.

- Phase 1: Localization. Establish your Kabushiki Kaisha and secure a physical office.

- Phase 2: Infrastructure. Implement the cold wallet system and ensure you can audit it in real-time.

- Phase 3: Compliance. Build out your AML/KYC pipeline and draft disclosures that meet FIEA standards.

- Phase 4: Application. Submit your registration to the FSA and prepare for an exhaustive audit of your internal risk controls.

The cost of this process is high, but the payoff is a level of legitimacy that few other jurisdictions provide. In a world where exchanges vanish overnight, being an FSA-regulated entity is a powerful marketing tool that signals stability and trust.

What happens if an exchange operates in Japan without FSA registration?

It is strictly illegal. The Japanese government takes a no-nonsense stance on unregistered operations, and companies attempting to bypass the registration process face severe legal penalties and an immediate ban from the Japanese market.

How much of a user's crypto must be kept in cold storage?

By law, crypto-asset exchange service providers (CAESPs) must keep at least 95% of customer assets in offline cold wallets to prevent theft and hacks.

What is the difference between the PSA and the FIEA in crypto?

The Payment Services Act (PSA) treats crypto as a payment method. The Financial Instruments and Exchange Act (FIEA) treats crypto-assets-specifically those with investment or governance features-as securities, requiring much stricter disclosures and market conduct rules.

Do I need a physical office to get a Japanese crypto license?

Yes. The FSA requires a physical presence within Japan, a local Japanese bank account, and a registered legal entity (typically a Kabushiki Kaisha).

Are crypto taxes in Japan being reduced?

The FSA is currently advocating for reforms to move crypto taxation away from the "miscellaneous income" category (which can be up to 55%) and align it with the lower flat tax rates used for stocks and bonds.